Graphical travel user interfaces (GUIs) such as agent desktops, online booking tools and mobile interfaces have been around for a while by now. While they are pretty successful in the online booking space with an adoption at around 90 percent, they are still lagging behind with agents who love their cryptic screen or “green screen”, how this terminal access is called by insiders referring to the ancient IBM 3270 terminals.

Agents claimed to be faster with their cryptic screens where they do not need to take their fingers off the keyboard to use a mouse. However, providers such as PASS that started with graphical agent desktops already in 2003 proved in trials with almost all major TMCs that with graphical screens, the times to complete bookings are comparable, if not faster. Using the PASS agent desktop, no agent needs to take their fingers off the keyboard, following the principle: whatever you can do in cryptic, you should be able to copy to GUIs as well. It is true that an agent might lose some time until the first results show up. But the rules and intelligence showing only what is relevant for this specific traveler along with automated file finishing rules make up for this time lost and even save some more time. A fact confirmed by a TRX executive.

It’s all about the money

Many agents were reluctant to adopt a new technology because, first of all, that meant change and many people don’t like change. But, more importantly, it made them more exchangeable. Their “USP” of being fast with cryptic commands became obsolete and almost anybody who knows how to book a trip on Expedia can now with minimal training be an agent. In 2010, sophisticated agent desktops were even source-agnostic – meaning that the user interface looked the same in different GDSs. From a technology perspective, it is easily possible to combine and aggregate sources, e.g. content from different GDSs with low cost carrier content and direct connect content. Needless to say that GDSs didn’t like that fact very much and therefore, as confirmed in the US Airways/Sabre trial, prohibited technology providers to market their tools: “Controlling the interface is a strategic imperative for Sabre” (paywall), documents Jay Campbell in The Company Dime. As it came to light now, similar to PASS, Concur was prohibited to use a multi-source agent desktop unless it was grandfathered by Sabre. Large TMCs such as American Express GBT were able to secure initiatives such as their multi-source agent desktop in Canada provided by PASS Consulting and Farelogix to supplement GDS content with Air Canada’s direct connect and Via Rail content.

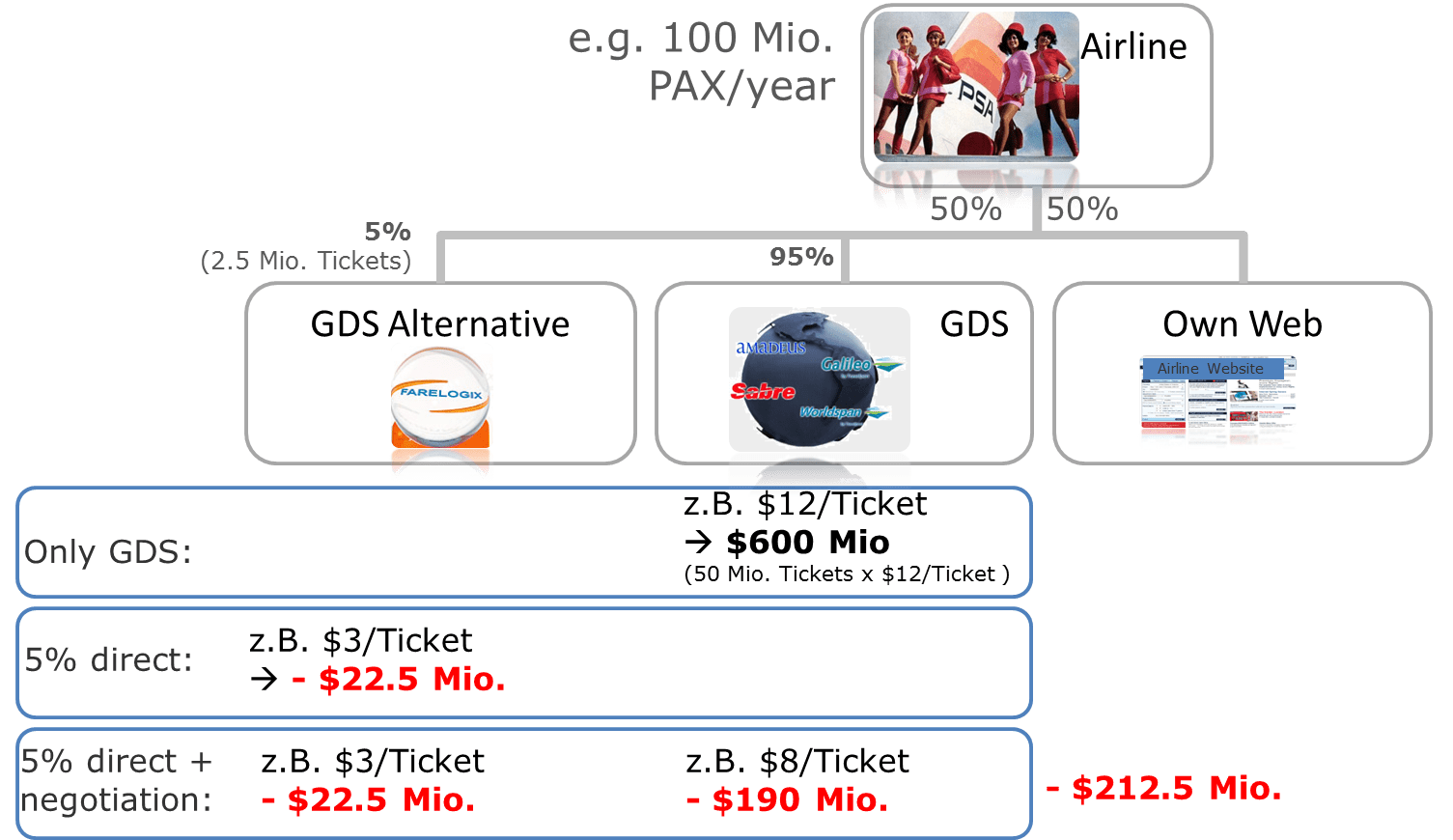

Obviously, the top TMCs could have started a fight with the GDSs but considering commissions and overrides received from the same, this was unlikely to happen. According to The Company Dime (paywall), in the seven years between 2006 and 2012 those TMCs alone received $ 1.2 billion in incentive payments by Sabre alone (GBT: $ 504 m., CWT: $ 493 m., BCD: $ 184 m., HRG: $ 43 m.). This translates into a per-booking average of $ 2.65 to American Express GBT, $ 2.71 to BCD Travel, $ 2.44 to Carlson Wagonlit Travel (CWT) and $ 2.10 to Hogg Robinson Group (HRG).

It appears that in order to put those fees TMCs received from Sabre (paywall) into perspective, it was also indicated that in the United States, 63 percent of GBT bookings were made on Sabre while for CWT it was 82 percent, for BCD 65 percent and for HRG 97 percent. While it seems impossible to calculate the exact Dollar amounts which changed pockets on a worldwide scale for each GDS and TMC, I still believe one can get a good sense of the magnitude. For a TMC it would have been a tough call to start a fight with somebody who pays them up to $ 1.2 billion per GDS in that timeframe – especially if all these players have the market power to shift business to the competition.

All figures at one glance

| GBT | CWT | BCD | HRG | Total Big 4 | |

|---|---|---|---|---|---|

| Commission & overrides to top TMCs 2006 – 2012 [$ millions] by Sabre (worldwide) | $ 504 | $ 493 | $ 184 | $ 43 | $ 1,224 |

| Share of Sabre vs. other GDS bookings (US only) | 63 % | 82 % | 65 % | 97 % |

While it becomes pretty clear why TMCs and GDSs rather wanted to preserve the status quo, looking at it from an airline perspective, it is also clear why every five years, when full-content deals are back on the table, there are ambitions to threaten with direct connect deals – even though eventually they end up in an agreement between all parties. As I mentioned in my book Value Creation in Travel Distribution, it is all about negotiation power.

Large investments

Investment in graphical agent desktops, as it was revealed in the Sabre/US Airways trial as well, were $ 20 million at BCD Travel for Renaissance (abandoned in 2009), $ 10 – $ 15 million annually (!) at CWT to develop, operate and maintain Symphonie, and at American Express Global Business Travel (GBT) around $ 100 million for TravelBahn Gateway (a single GDS desktop with limited content aggregation). Online booking tools even require higher investments: Concur invested around $ 2 billion over the years, which suggests that a minimum of $ ½ billion went into the booking portion of Cliqbook.

While I won’t disclose the exact investment we at PASS put into our graphical travel user interfaces, they also go well into the tens of millions of dollars. The slight difference is that our GUI is future proof as our development is based on newest technologies. During our trials after 2007, we realized that for major TMCs, one size won’t fit all and did a complete overhaul. The architecture now is completely SOA-based. Individual tools can be created built-to-order in accordance with any client’s requirements based on re-usable components. In addition, we integrated an open source rules engine which puts the clients in the driver seat. The major advantage, however, is the fact that it is not an agent desktop only (or an online booking tool), but actually both based on the same architecture. If you improve something or create a new feature, it will benefit all interfaces – be it the agent desktop, the OBT, or anything else to be created in the future (mobile apps, chatbots, virtual agents, etc.).

Picture Credit: shutterstock, Value Creation in Travel Distribution by Michael Strauss

This Post Has 4 Comments

[…] as you can see in my picture about airline commission and overrides, that besides fees for fuel, staff, aircraft, technology, credit card fees etc. the ticket price […]

[…] the mix. How can this be done? The financial relationship between GDSs and TMCs for example is a multi-billion Dollar relationship. There are many who do not like change and definitely not if the change costs money and it is […]

Dear Jay,

Many thanks for watching out that the facts are reflected correctly. I changed the numbers in the article accordingly. Now, I left it to the reader to guess how much TMCs received from GDSs other than Sabre. Bottom line in my eyes is, that these lucrative deals will decrease for TMCs in future (now that these numbers became public). Thus TMCs (or corporations) are invited to invest in their own technology, which they can easily do thanks to another article you wrote: TheCompanyDime: http://www.thecompanydime.com/online-booking-tool/ (reprinted with permission on: http://bit.ly/1Xxwf5J).

Best,

Michael

Thanks Michael for highlighting our coverage.

One comment on the numbers. This is not correct: “It was also indicated that those fees TMCs received from Sabre accounted for 50 percent of all incentives and overrides GBT received, while for CWT it was 82 percent, for BCD 65 percent and for HRG 97 percent.” The article reports Sabre bookings as a percentage of the TMCs’ U.S. (not global) bookings. That’s a very different geographic scope. Also, although it’s close, the percentage of bookings does not match the percentage of incentive money since the different GDSs pay TMCs different rates. It appears that you extrapolated from that data to determine global totals for all GDSs. I’d say the numbers you came up with are substantially undercounting, especially for HRG.

By the way, we have since updated one of the articles you referenced with more detailed estimates of BCD’s and HRG’s intake from Sabre: http://bit.ly/2hFOZCu