In October 2017, I wrote a blog about the technical and commercial challenges of NDC. The title was “The reality behind NDC: Why NDC won’t break down the GDS oligopoly – yet”; A year later, I guess one can say for sure that the last word “yet” of the title can be erased. The New Distribution Capability – or in short NDC – will come that’s for sure, but primarily through the GDSs!

There may be a few island solutions on direct connects, but each GDS has committed to NDC. Sabre caught up with an acquisition of former rival Farelogix for $360M – a player who provides NDC capabilities to airlines such as Lufthansa based on PASS technology XX1. Amadeus reached NDC Level 3 certification in July 2018, Travelport claimed to become the first GDS operator to make a live NDC booking in October 2018 [Remark: we at PASS have issued tickets before, but just didn’t feel it was important to brag about it.]So, all in all, I believe it was the right decision for us to not jump the gun and develop numerous NDC connections ourselves. We did one with Lufthansa in one of our home markets, so that we know what it means and what it takes, but otherwise we waited while GDS indeed shifted their gears from being opposed to NDC to becoming a supporter.

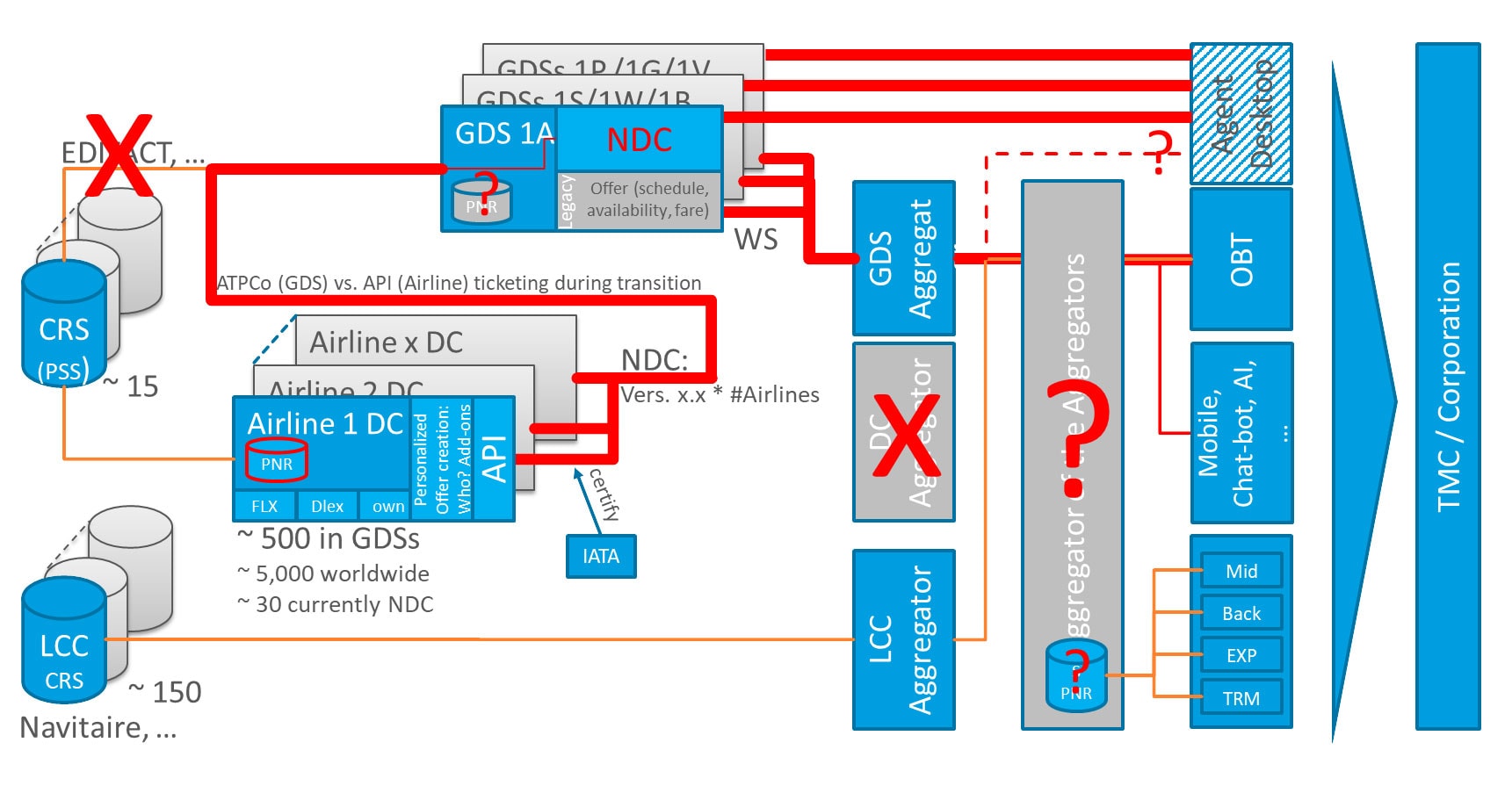

Using the graph of my 2017 blog, I’d like to showcase, what has changed in a year and remind you what NDC really is:

NDC is a standard to which airlines can build their API (Application Programming Interface), which you can see in the graph: Airline API. It is based on XML (the 1st version was actually our XML), which is a language becoming widely successful around the year 2000 to replace an earlier communication language between airlines and providers called EDIFACT (which came out in 1980s) – top left in the graph. I’m always joking, that essentially 40-year-old technology is replaced by almost 20-year-old technology and that is considered “New” Distribution Capabilities. However, an API needs to have a robust schema and XML brings that to the table.

Along with NDC, airlines are also changing the shopping process: previously an offer was created by the GDS based on fare, schedule and availability, in NDC, the airline creates the offer and with that can also provide add-ons such as Wifi, lounge access, pre-boarding and other things based on “who is asking”. In other words, it also allows to personalize offers. It can also mean that a company negotiates with an airline special conditions for certain executives. Finally, it may help with data collection as well. This is shown in the graph in the airline rectangle and greyed out in the GDS rectangle (which GDSs may still have to do for legacy carriers not speaking NDC). So, GDSs have to find a way to mix and match regular carriers with NDC carriers.

Really? A Standard?

In short: NDC is supposed to be the plumbing behind the supply chain that enables a consumer like travel experience – the one you experience on the airline website.

But people may argue (including myself as a technology provider who regularly has to sign off on the time sheets our developers spend) that we are not there yet. In 2018, NDC is not widely considered a standard. The XML schema may be a standard, but implementations and offerings vary from airline to airline. Some include interline, some not, the form of payment is always a fun part, and exchanges is a topic by itself.

A person from IATA, to some extent agreed and told me that ‘with early adopters there is always chaos, but with 17.2 (the 2nd NDC version of 2017), GDSs & IT companies agree, we are ready for industrialization. Going forward, there will be two new versions per year in the future, however, these will be just evolution.’

As it appears each airline has their own interpretation of NDC and developed their own customized API. Which means essentially what I mentioned in my former blog, every integrator (i.e. every GDS) may have to integrate potentially up to 500 airlines separately which is impossible. Up to this time, airlines were at an all-time high. Load factor is close to 100% continuously. Airlines publicly claimed they will never lose money again. Somebody said that airlines have a tendency to ignore what IATA put into place. How do you get them to respect and ensure that one interface looks like the other one? Now, that the GDSs are on board this may change and respect may come, but obviously on the flip side it also slows progress down again. So, the battle might go on.

The question becomes, couldn’t we have it much simpler such as airlines and GDSs locking themselves up in a room to figure out the future instead of bringing out the artillery and making a lot of people nervous? I asked that question to my panel of two airlines, one GDS and a partially impacted party as part of the CAPA World Aviation Outlook Summit in Berlin, but other than ‘we tried’, I didn’t really get an answer. Sometimes things have to be forced through apparently, it just reminds me again that the industry might be so busy with battling their mini-wars that we may overlook how to improve the overall travel experience for the traveler. Decades ago, air travel was something interesting, something exciting, today, in the western hemisphere it has become a burden, with all the security, more people being squeezed in seemingly smaller spaces of an aircraft, constantly full and overbooked airplanes, unions in Europe regularly on strike, volcanos, you name it. There are many things that can be improved and now being able to pay extra for a previously included feature may not be what the traveler was desperately waiting for. At the same time the fare has not really come down on highly frequented routes over the past decade and a half. If there is a vacuum of improvement, usually somebody will eventually step in – like Apple revolutionizing the music industry when the industry itself was too busy fighting illegal downloads (Napster, etc.).

Is Airline IT-Infrastructure ready for NDC?

I also asked my panel about speed and performance. The old legacy systems had two advantages: developers who (still) cared about effective programming & performance and lightning fast speed at minimal memory consumption. Several airlines committed to the IATA leaderboard target of 20 percent of their indirect sales (excluding airline.com bookings) through NDC by 2020. Some GDSs confirmed they are on track to reach that number. However, today I’m sure less than 1% of that envisioned volume is actually booked through NDC channels. This means realistic live system performance data is unavailable. Consequently, performance may become an issue once usage picks up. My panel did not see this yet as a threat (yet). They also argued that the shopping process is changed: results will not consist of all connections between A and B, but rather a subset of a specific preferred carrier based on personalized factors. Today a GDS searches all possible connections with all possible carriers and combines an offer of approx. 200 in the GDSs‘ eyes, best results (using Bargain Finder Max from Sabre for instance); with NDC an airline could drill their offers down to less proposals which in the airlines‘ eyes match the traveler‘s preference better and consequently the GDSs have less offers to collect. If everybody plays by the rules, indeed, it could mean that less is more. I‘d like to see it first. Airlines may also become creative to outsmart their competition – as they do today: schedule the take-off a minute earlier to be better ranked than the competition.

Airlines trapped between GDSs? What is the future role of TMCs?

What is going to change after the Sabre/Farelogix acquisition? Not much, other than it is clear that the GDSs will join the party. Lufthansa who has been using Farelogix with the goal to achieve a better negotiating position and to escape full content and content parity agreements is now trapped between the claws of two GDSs: Sabre NDC on the API side and Amadeus Altea on the CRS side. Lufthansa, however, kept calm by saying they already have backup players (i.e. Datalex).

While GDSs definitely will need to force standardization of NDC in order for them not having to integrate up to 500 airlines separately (again), another battlefield will be happening on the commercial front: an agreement with each airline has to be found. As long as GDSs already have an agreement with such airlines today, it seems to be just another topic on the agenda when it comes to renegotiations. This may be a different topic for newly emerging NDC aggregators – something the airlines probably bank on to get a good deal. However, a bigger item may be, what you are entitled or not allowed to do. NDC aggregators (or those who use NDC aggregators) need to carefully read their agreements. In the press I read many times, to just use passive segments for post-booking services. But rarely those passive segments come free of charge, and sometimes one may be prohibited to use a passive segment. This means we may be right back to the challenges of my NDC blog from last year.

The new constellation has an interesting flavor among GDS themselves: for instance, a Lufthansa NDC booking using Sabre/Farelogix NDC offer management ends up on the Amadeus Altea CRS, could have been distributed via a Travelport GDS. This brings all competitors of the oligopoly in touch with one and the same booking. So, who owns the booking? Who is entitled to share or sell the PNR information? Especially the interface between the NDC API and the GDS may need to be unbiased. An aggregator of several GDSs and direct connects may also need to be able to access each system without restrictions.

Let’s go a step further and include agencies and Travel Management Companies (TMC): Today, the job of getting an offer right sits with the GDS/TMC. With NDC the balance of responsibility shifts to the airline – even during the trip. It becomes especially interesting when interline partners are involved. Even though an Offer Responsibility Airline (ORA) has been defined in IATA’s NDC. Now, combine a trip of legacy carrier with NDC carrier both to include interline segments – good luck! Something goes wrong, who is to blame? TMCs are in the first line of defense. Will TMCs be able to easily blame the airlines? Or will the corporation hold the TMC responsible no matter what? Even more interesting when it comes to Travel Risk Management / Duty-of-Care! TMCs have claimed that reporting as well as duty of care is something, no airline has figured out. However, the airline members of the panel looked surprised by this statement, had they not invested in connectivity to some of the major mid- & backoffice systems. This might be true for some installations, but from what I hear the majority corporations seem concerned about the servicing capabilities after the booking was made.

Everything great with NDC?

It is claimed that NDC promises big changes, as stated e.g. in Business Travel Executive’s Dec. Issue, reduces costs and creates a better, meaning consumer like, user experience, such as better content and better distribution. Obviously, NDC offers more selling capabilities than cryptic codes. So, we can checkmark that, however reducing costs, when at the same time fundamental changes have to be made on how airlines, GDSs, agencies/TMCs and booking tools work together seems a little off. We should not overlook that every sales entity at the same time is also facing market challenges such as providing a competitive user interface (mobile, bots, speech, artificial intelligence, etc.) – not to even mention any technology advances such as blockchain (it usually gets very quiet once somebody mentions that word). It is tough to be forced to work at the plumbing, when at the same time you have to ‘wow’ the users with consumer like user interfaces.

The airlines see NDC integration as an investment into the future. The first EDIFACT versions also required a lot of finetuning and efforts were made to make it work. Better plumbing for a better and futureproof user interface? I can relate to this statement but it is a tough pill to swallow for the ones affected. And it brings me back to maybe somebody outside the industry has an easier way to manage. I guess, we have the luxury that booking travel is really something very complicated to do. I recently asked one of my developers who came from Groupon during a discussion about modern vs. legacy programming methods (and this is not dating back to EDIFACT age, rather just one decade to XML vs. REST and programming in small services rather that big elephants), if our software in travel is so much more complicated than a feature set companies such as Groupon provide? He confirmed that travel is way more complicated! This made me feel good about our industry, who was once at the forefront of IT! Probably one of the first industries to really use IT for a business purpose. And rightfully so, now we have to catch up, arrive in the present and be a leader of the digital age again.

So, now that we have GDSs on board, we know that big changes to the technology but also to the commercial model have to be made, and we know, we need to include the TMCs into the mix. How can this be done? The financial relationship between GDSs and TMCs for example is a multi-billion Dollar relationship. There are many who do not like change and definitely not if the change costs money and it is unclear who is going to pay for it. There is also concern about cutting out the middlemen. At the same time, the corporate buyer as well as the consumer is more knowledgeable than ever and we need to respect that. How can this work? On the panel the answer was presenting some intentions, such as that BCD Travel just announced an NDC pilot with Lufthansa, and that we will see more such news. However, between the lines what I heard is that the TMCs rather wait until the GDSs deploy solutions. I also understand that the TMC’s role in the value chain mainly consists of supporting the traveler during the trip.

While suppliers are looking at a closer relationship with their buyers and influence their shopping decisions – a trend towards direct connect, nobody wants to cutout the middleman. How could this work? According to an IATA paper the four areas of travel buyer needs are:

- Customer – removing traveler dissatisfaction with UX (user experience)

- Control – stopping lack of effective control on content & channels

- Care – plugging the inability to provide appropriate duty of care for their travelers

- Cost – curtailing lost savings and lots of time spent on dealing with issues.

So, what should TMCs do? The IATA paper provides the following answers:

- GDS based IT: waiting out existing provider readiness (aggregation & agency desktop) – moving slower because of large and complex IT, current incentive model

- Other 3rd party-based IT: want to evolve IT & commercial model, using 3rd party providers – sense of urgency due to content differentiation

- Insourced IT: Consider themselves as IT player and have built own platform – moving fast, new commercial models, addressing NDC opportunities

Who will pay for managing all these challenges? Airlines mentioned that those who add value will be compensated, but it was unclear if the current commission & override model will sustain.

In the end legacy airlines able to compete with low-cost carrier, but GDSs once again rule indirect distribution!

In summary, I think we are back to the future. All the roles in the value-chain of business travel have been established and remain established. The legacy carriers (at least some of them), with NDC were able to force a new selling paradigm into the industry which allows them to better compete with the low-cost carriers. From an airline’s perspective, this is understandable: While business travel once provided the profits of a legacy carrier, today, the back of the plane accounts for “¾ of the revenues” according to Carsten Spohr, Lufthansa. The most profitable airlines are low-cost carrier (e.g. Southwest) or even ultra-low-cost carrier (e.g. Wizz Air) and NCD gives legacy carriers a method to compete. However, it seems to be a lot of smoke for a small outcome. The whole process could have been handled much easier, if all players worked together. I’m not even sure if there is a winner or loser in this battle. A lot of headache on all fronts: airlines, with huge investments and fighting PR battles, GDSs also with huge investments and coming across like an elephant not willing to move where Sabre in the end paid a seemingly overpriced price tag to catch up, and TMCs for a long time not knowing which side to settle on and failing to be considered a part of the equation. A little understanding for the other side would have saved a lot of money and nerves. And the corporate buyer would have probably been a little less annoyed by the active actors.

Key ideas of NDC:

- Provide commonality, simplicity and lower barriers of entry.

- Product differentiations such as fare families.

- Identified travelers vs. anonymous travelers.

- Ancillary products provide airlines an opportunity to differentiate themselves.

- Consumer like shopping experience in indirect sales channels.

- Ability for legacy carrier to compete with low-cost and ultra-low-cost carriers.

- Meet traveler demand for relevant services throughout the journey.

- Sell additional services though NDC to complement existing fares with optional à la carte products.

- Most ancillary products and services can be sold separately or attached to a flight. They can then be bundled together to create a product bundle. The most common type of a bundle is the fare family.

- NDC message can also carry images and text to complement an airline‘s service and inspire the traveler.

Travel XML API

Picture: Shutterstock

This Post Has 20 Comments

Dear Bo & SL,

Let me see if I can answer your question to your satisfaction:

1) ATPCO indeed has the fare information filed by the airline. You still need to have access to real live inventory. With NDC that is probably the case bypassing GDSs. One would still need an agreement with the airline in order to be allowed to access their NDC content. However, the concept of creating a booking with NDC is somehow slightly different: With GDS the GDS creates an offer based on such pre-filed fares of respective fare classes (class Y, class C, etc. – the number of such different classes are actually limited by the alphabet). With NDC the airlines create the offer based on several real-time factors such as current load factor and whatever else airlines can do to maximize profit (yield management). As an example: if the very restricted business class P fills up, today, with the current method of GDS offers, you need to jump to the next higher class (e.g. Z or if that one is filled even C), which means a huge price jump just because the last seat (inventory) of the P class was taken. In future with NDC the airlines are planning a more linear increase in prices instead of this step-by-step increase. This means airlines can dynamically price their offers based on demand and supply instead of the limited 26 fares that have filed with ATPCO a year in advance . So, while in principle you are right, the airline idea behind the commercial model of NDC goes one step further.

2) Google flights is based on ita-software which Google acquired several years back. Ita-software together with G2 Switchworks (acquired by Travelport) and Farelogix (now to be acquired by Sabre) were the so called GNEs (GDS New Entrants). Ita-software had a very sophisticated performant flight search algorithm which was used by many airlines themselves. Hence, they have very good relationships with airlines. I’m not sure about the commercial model today, but in the past metasearch engines incl. Kayak, sidestep (today also Kayak), etc. received a commission when the directed the clients to the respective booking sites. I think, one estimated that the acquisition of one client is about $17, while the fee to a metasearch engine is about $5. So, it is supposedly a non-brainer. However, in my eyes it lacks the realization that with this model one has to “acquire” the same client over and over again, because he/she will always use the metasearch engine as an entry point again. Something like this was Amazons biggest challenge that people shop on Google and then get transferred over to Amazon, instead of starting their search already on Amazon.

I hope this helps a little bit .. but I’m open to any critical feedback or comments.

Thank you,

Michael

Bo, Great questions.

Michael, I’d be interested as well.

Thank you, great blog!

Hi Michael,

Great and informative article. Thanks for posting. I have a few questions if you don’t mind:

1) If all the airline fare information is posted through ATPCo. and scheduling information posted through OAG or whomever, why can’t someone like an OTA, who already aggregates to some extent I think, direct connect into the ATPCo. or OAG and bypass the GDS? Is it because they don’t have the ability to process a booking? Wouldn’t level 3 NDC solve that?

2) Do you happen to know where Google Flights sources is supplier data from? What does the model look like there if its not using a GDS? Does the airline just pay them a commission for them to aggregate flights and redirect customers to airline sites? Are they using ATPCo information?

Thanks in advance.

Thank you! I appreciate the kind words!

Marvelous work! Blog is brilliantly written and provides all necessary information I really like this site. Thanks for sharing this useful post.Thanks for the effective information.

Hi Michael,

Thank you for the informative article.

One related questions if you could please help with- How do you see Content/Experience Management Solutions (e.g. AEM, Sitecore etc.) helping in this complex airline landscape and in which part-

1. Offer creation

2. Offer deliver

3. Shop

4. Book

5. Ticket

6. Check-in

7. Manage booking

8. User behavior data capture

9. Personalization

Thank you in advance.

Dear Timothy,

Your best bet is through IATA.

Some potentially valuable information can be found (at the time of the writing of this comment) on https://www.iata.org/whatwedo/airline-distribution/ndc/Pages/default.aspx. Schemas can be found (at the time of writing of this comment) on https://www.iata.org/whatwedo/airline-distribution/ndc/Pages/schema-description.aspx.

I hope this helps.

Thanks,

Michael

How can we get the specs for NDC?