Even if airlines only had a single price for each cabin (first, business and economy), the price per cabin would still be high.Consequently, only a few people could afford to fly, which would lead to inefficient capacity utilization as no-one would be able to determine how much an optimal price would need to be in order to fill up the aircraft – a nightmare for an airline’s yield management.

From Single Pricing to Static Offer Creation to Dynamic Pricing to Continuous Pricing

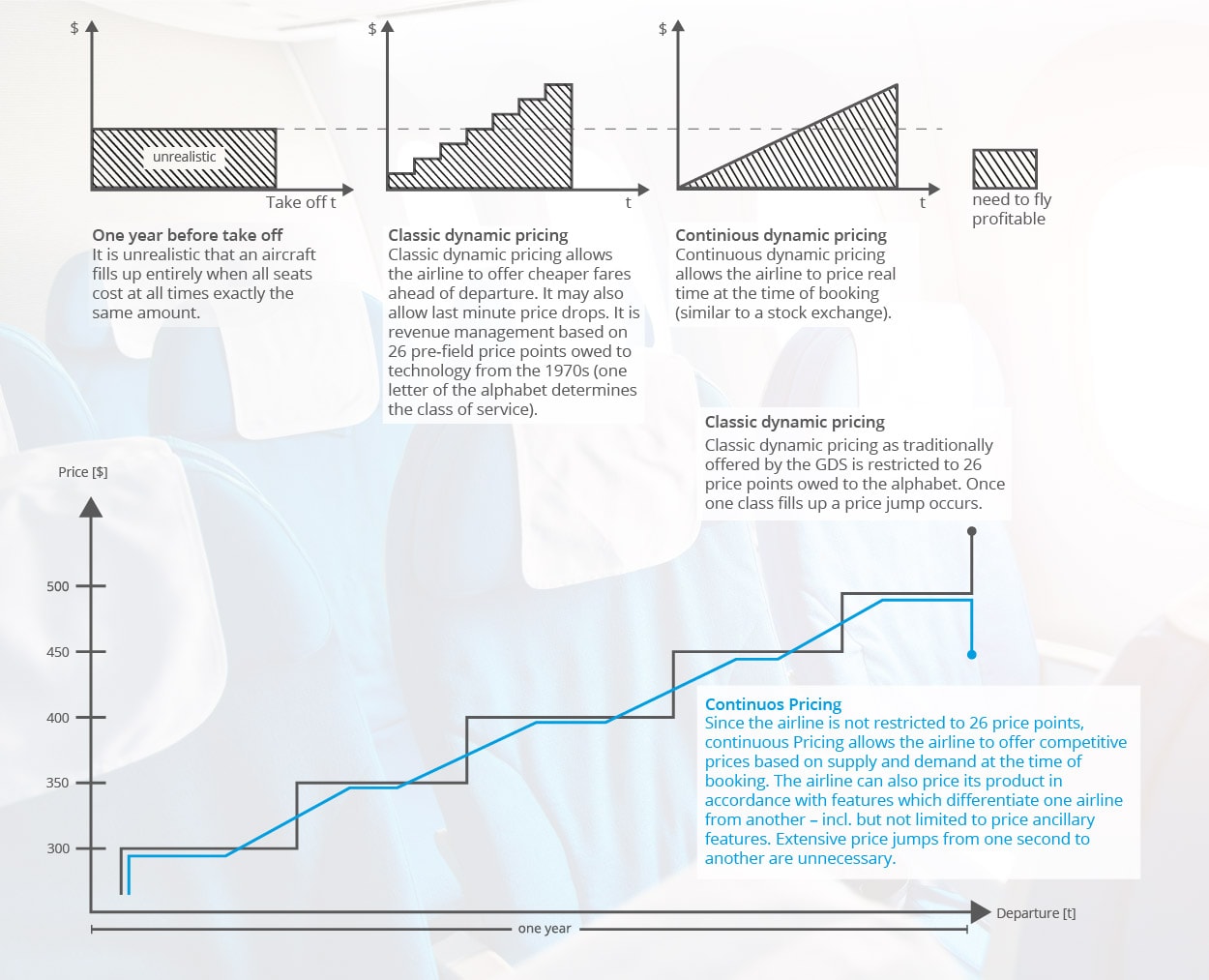

In order to fill up aircraft at an economical price per ticket, this led to static offer creation with booking-class based dynamic pricing: For several decades, airlines have filed their booking classes with ATPCo. These booking classes where historically limited to the alphabet, so we have up to 26 booking classes divided into 3-4 cabins, known as for instance A or F for the First Class cabin, C, D, or J for Business Class cabin, E, G or N for Premium Economy cabin and B, Y, H, M, U, Q, S, V, W, K, L, T for Economy class cabin.

Each booking class has pre-filed rules, such as the possibility and fee of a refund or rebooking, included baggage, factor for mileage accrual, restrictions and other items – again, all this had to be filed in advance and depending on available inventory of each booking class the GDS prepared the offer to the traveler. The advantage was that many passengers were now able to buy tickets for low fares for instance early, last minute or with certain restrictions, which led to the fact that airlines were able to offer more profitable connections by using the capacity more efficiently and consequently were able to accommodate passengers with short-term travel needs who were willing to pay a premium.

Blog Series: Travel Technology for Dummies

- What Is Full Content?

- What Is a Booking Reference or PNR?

- What Is Overbooking?

- What Is a Passenger Service System (PSS)?

- What Are Booking, Waitlists, Tickets, Codeshare & Interlining?

- What Are Active and Passive Segments?

- What Are Incentives, Commissions & Overrides?

- What Is a ‘Married Segment’?

- Blockchain in Travel: All You Need to Know – for Now

- What Is the Difference Between Fares, Rates and Tariffs?

- What Is NDC?

- What Is Continuous Pricing?

- What Is Direct vs. Indirect Distribution?

Airlines Claim: “NDC Avoids Unnecessary Price Jumps for Travelers”

One step further with NDC, some airlines propose what is called “continuous pricing”: The traditional pricing in the GDS dates back to the 1970s with its limitation to 26 pricing points. Airlines argue that this causes unnecessary price jumps for the travelers, but also prevents the airline from materializing profits as certain classes fill up. Price jumps can sometimes be seen when you search for one person and get a fee of e.g. $120. Then you try to book for the whole family and now all tickets jump up to $180 – as you, potentially together with some family members, filled up the cheaper class. I ended up booking separate tickets in the past to at least take advantage of some tickets at the still lower rate – but that’s a dangerous move, especially if plans change.

Being limited to 26 price points, puts the indirect sales channel (via agency/GDS/NDC) at disadvantage to the direct sales channel (airline website). On the airline.com website, one may find real-time fares based on supply and demand fares, while the traditional channel is restricted by the alphabet. Continuous pricing may allow airlines to offer more competitive pricing across all channels, as price jumps can be reduced significantly not just in direct sales but also in the indirect distribution channel alike. Unless all channels are capable to display continuous pricing, price differences between distribution channels (e.g. travel agent vs. airline.com website) occur which will favor the airline.com website, confuse the traveler and put agents at a disadvantage.

| Static pricing | Classic dynamic pricing | Continuous pricing | |

|---|---|---|---|

| Key difference | One price per cabin | Limited to 26 price points step-by-step mathematical model | Unlimited amount of prices continuous mathematical model |

| Distribution channel and technology | Unusual / not existent | GDS (EDIFACT) / ATPCo filed fares, OAG/innovate filed schedules | Airline API / NDC XML |

| Pricing based on | N/A | Origin/Destination, trip characteristic, rates, compartments (cabins), services & ancillaries (bags, meals, leg space, demand forecast, load factor, etc. | Origin/Destination, trip characteristic, rates, compartments (cabins), services & ancillaries (bags, meals, leg space, demand forecast, load factor, etc. |

| Pricing not based on | N/A | Sensitive user data due to GDPR compliance: traveler income, mobile data, monitoring data, browser data, gender, ethics, etc. | Sensitive user data due to GDPR compliance: traveler income, mobile data, monitoring data, browser data, gender, ethics, etc. |

Pictures: Shutterstock, PASS

This Post Has 2 Comments

Dear Ian,

Thank you for the further insight. I agree with you that there are always ways to circumvent restrictions and that airlines have been very creative in the past to overcome those restrictions all the way to branded fares / fare families. And when it is convenient to justify an imperfect move to NDC (compare https://www.travel-industry-blog.com/travel-industry/ndc/) & continuous pricing airline may argue the other extreme: “We only have 26 price points” or as I recently learned actually just 23 as there is no O, I or X – or if you follow an old joke only 20 if you agree that KLM just took off (credits to Timothy O’Neil-Dunne).

The more price points you have the less comparable they are. Even with branded fares one may already need an (expensive) subscription to ATPCo’s Routehappy with all the Classes of Service (CoS), ancillaries (https://www.travel-industry-blog.com/gds/ancillary-revenues-blessing-or-curse/), or EMDs (http://www.travel-industry-blog.com/gds/the-beat-live-ndc-tmcs-buyers-deja-vu/) to somehow provide an informative choice to the traveler.

Continuous pricing coupled with CoS, branded fares, etc. seemingly just makes it impossible to compare it all, while providing maximum flexibility to the airlines. In the end the golden path lies in the middle and provides some flexibility to the airline, but also provides some kind of standard. Let’s not forget that it is a bad idea to screw the traveler and if I book a business class seat, all happy that I saved a few bucks, just to find out that it’s not even a lie-flat seat – that airlines will be banned for life. We are in an age of incredible technology – and make no mistake one will figure out how to compare apples to apples. We (aggregators) just need to provide them with access to all content.

The article itself is just trying to inform, but it’s great if we start a whole discussion forum here… pls. keep it coming.

Thanks,

Michael

Thanks for the good article Michael, very informative as usual. My only question is over the assertion that in the classic dynamic pricing model airlines are limited to 26 price points. In practice they’ve always had the ability to use fare basis coding to provide different fare levels / rules within the same prime RBD / booking class letter i.e. minimum advance purchase , Saturday night stay, day of week, length of stay etc. Plus of course many have their fare families which provide further differentiated price points within the same RBD.

As such I’ve always thought the airlines have been slightly disingenuous using the ’26 price point limit’ argument to advance the case for continuous pricing. Like you I’m concerned about further fragmentation of content between channels, even as NDC capability to deliver through the GDS comes on stream. Until we see it fully in action I remain somewhat cautious on this for the corporate client base I represent, from a transparency and benchmarking perspective at least.