Dear Readers, during a tough year with a global pandemic which cost the travel industry according to IATA in excess of $118 billion, I was under the impression, no-one would be interested in educational stories about travel technology. Hopefully, we have better times ahead of us. Hence, I decided to continue my series with focus on necessary technology improvements such as NDC and ONE Order.

NDC is to become the standard for airline distribution of the 21st century. As mentioned in my article about NDC from Oct. 2017, NDC is the replacement of a communication protocol from the 1980s (EDIFACT) by a communication protocol of 2000 (XML) – which basically means data becomes more readable. The reason behind this development: Every data element gets a description of what it stands for (you can find out more about that in the other articles of this series).

Blog Series: Travel Technology for Dummies

- What Is Full Content?

- What Is a Booking Reference or PNR?

- What Is Overbooking?

- What Is a Passenger Service System (PSS)?

- What Are Booking, Waitlists, Tickets, Codeshare & Interlining?

- What Are Active and Passive Segments?

- What Are Incentives, Commissions & Overrides?

- What Is a ‘Married Segment’?

- Blockchain in Travel: All You Need to Know – for Now

- What Is the Difference Between Fares, Rates and Tariffs?

- What Is NDC?

- What Is Continuous Pricing?

- What Is Direct vs. Indirect Distribution?

The Bumpy Road to NDC

The road to NDC was bumpy as a technology standard was used for political reasons: NDC was confused with direct distribution (airlines sells directly to traveler) compared to the classical distribution channel airline use GDSs and agencies for indirect distribution (compare with the picture from my article about PSS), where every entity in the value chain takes a cut of the sale.

Even prior to NDC, direct distribution was common – better known by booking through the airline webpage. On average 50% of sales of the classical legacy airlines, as well as up to 100% of low-cost carriers (such as Southwest), were sold through the website of the airline. Besides the above referenced article, I explained at length commercial challenges, people used to address using NDC as a weapon in my 2nd article about NDC.

At this point, NDC is (or will become) reality. Airlines effectively have been working on providing NDC interfaces since 2018 after IATA was able to provide a (to some extent) stable version with NDC version 17.2 (it’s the 2nd version of the year 2017). Approximately two versions will be released every year. GDSs have committed to providing NDC interfaces (NDC-X, Sabre Beyond NDC, and Travelport announced Travelport+). TMCs are engaged, but obviously rather prefer the traditional program with kickback for monetary reasons. Online Booking Tool provider are also somewhat engaged including SAP Concur and our own OBT.

Still Challenges Lie Ahead

However, as of 2021 we have still been facing challenges as there is no one-stop NDC provider. GDSs are releasing capabilities for a few airlines each year. While some aggregators claim to have numerous airlines, in many cases the fact is, they only have a few real installations. Aggregators claim for instance to have Austrian Airlines (OS), Lufthansa (LH), SWISS (LX), Air Dolomiti (EN) and Brussels Airlines (SN) while all of these airlines are from the same Lufthansa Group Application Programming Interface (API) – it is exactly one and the same interface.

Additionally, Lufthansa’s technology provider of the NDC interface is Accelya’s Farelogix. And Farelogix is the technology provider for other airlines, too – among those, besides the Lufthansa Group, Aeromexico, Aegean, Air Canada, American Airlines, Copa, Delta, Emirates, Etihad, flydubai, Hawaiian, Olympic, Qantas, Qatar, United, Virgin Atlantic, and WestJet. Theoretically and ideally, once you have integrated Farelogix once, one would expect to have all such airlines. The latter unfortunately is not true as we have different IATA NDC versions, different airline interpretations of such XML messages, in most cases we need a certification with each airline, and once all this has been taken care of, there is a good chance you run into bugs and/or technology limitations by the 3rd party IT vendor of the airline.

GDS Aggregator as well as a NDC Aggregator

Interesting is also that almost every aggregator pumps up their number of airlines integrated by mentioning each brand. For instance, the Lufthansa Group consists of the brands Lufthansa, Swiss, Austrian and Brussels airlines – it is still one adapter and you will get all 4 airlines. It looks much better on paper if you integrated four airlines. [Remark: Lufthansa also owns Eurowings, but Eurowings indeed is a separate not so easy to integrate Newskies adapter.]

Since 2021 PASS provides Travel Agent Desktop (TAD) – an independent and modern multi-source tool (NDC, GDS and non-GDS content) – for travel agencies.

Technical Challenges Should be Mentioned

Regardless, the claim to have all those airlines in one’s aggregator’s pocket is made quickly. But make no mistake, in order to have a comparable all-embracing offering as today’s GDSs, a new entrant “aggregator” needs to integrate up to 500 airlines, as I highlighted. If this was at all possible, it would basically mean to rebuild a GDS just using newer, more flexible but less proven and robust technology with questionable performance. As this is obviously not realistic, it will take time for NDC to get majority adaption and any NDC installation will need to be supplemented by a GDS aggregation.

- New integrations to up to 500 airlines,

- mid- & back-office challenges to manage a booking,

- Super-PNR database to manage bookings in various sources,

- unified agent desktop to modify or change bookings in various sources by a professional, and

- travel risk management (TRM) for bookings in various sources – especially TRM post-COVID.

Commercial Challenges Are Often Overlooked

NDC also comes with a number of commercial challenges, such as agreements between airline and NDC consumer (corporate, TMC, TRM, etc.) are necessary to get full visibility of all fares and features. Otherwise, the content is limited to zero or a “public NDC model”. In such a public model, an airline might make available limited content for those who do not have an NDC partner program agreement between the entity and the airline. The usual way is what some call “agency-paid” model, whereby an agency would first reach a bilateral agreement between the airline or airline group and such entity as part of a partner program, enabling access to all agreed NDC offers as part of such program. It is almost similar like public fares vs. private or negotiated fares in a GDS – where certain entities get access to certain negotiated fare of such entity.

The Biggest Change of NDC Is Shifting the Booking Responsibility From the GDS to the Airline

Apart from the communication protocol changing from EDIFACT to XML, the biggest change in the light of NDC is the change from a GDS created offer to an airline created offer. This is one of the prime factors for airlines to get out of their – as they call it – “commodity trap”, of reduced product presentation (no rich content – just a seat on a plane), no ancillary placement and no upsell options in their indirect distribution channel compared to the attractive product presentation on their own airline.com website along with filter criteria and upselling opportunities. Along with these restrictions comes: a static offer creation in traditional (GDS/ATPCO based) distribution compared to a dynamic offer management all the way to continuous pricing.

With NDC the offer and order model is introduced. The airline is in charge and provides the offer at the time of shopping. In addition to ancillaries, bundles, upselling, etc. this allows the airline to dynamically price at the time of shopping/booking as the airline is no longer limited to a tier model.

A more complete list of differences between the traditional ATPCO based workflow and the newer NDC based workflow can be found in the table further down.

NDC is

- XML based data transmission

- a revenue opportunity through XML based standard allowing product differentiation (see all drivers below)

NDC is not

- a commercial model (although commercial questions arise)

- a retailing solution

NDC Introduces Offer & Order Management

One of the Key Elements Proposed for an Airline NDC Platform is Offer and Order Management.

An offer management is part of the travel agency’s “NDC Shopping” request and triggers an offer creation by the airline dependent on information provided in the request. Also called “offer store” (as illustrated in the graphic further down), it enables airlines to distribute their full product offerings and to merchandise additional services using rich content (pictures, videos, sound VR experiences) in either an anonymous or personalized fashion. This may include dynamic pricing all the way to contineous pricing.

Order management is the ability to create, store and manage its orders. The order gives an entire view of the various products and services ordered. In a first step, a single identifier (Order ID) references to the PNR, e-ticket (ETKT) and EMDs involved in an order. The idea is that the order management becomes as sophisticated as in the retail world where the order is managed from purchase, payment to delivery. At some point in time, it is expected that order management is extended to cover the entire lifecycle, beyond fulfillment, to delivery and accounting. This is one aspect of the replacement of the PNR by ONE Order.

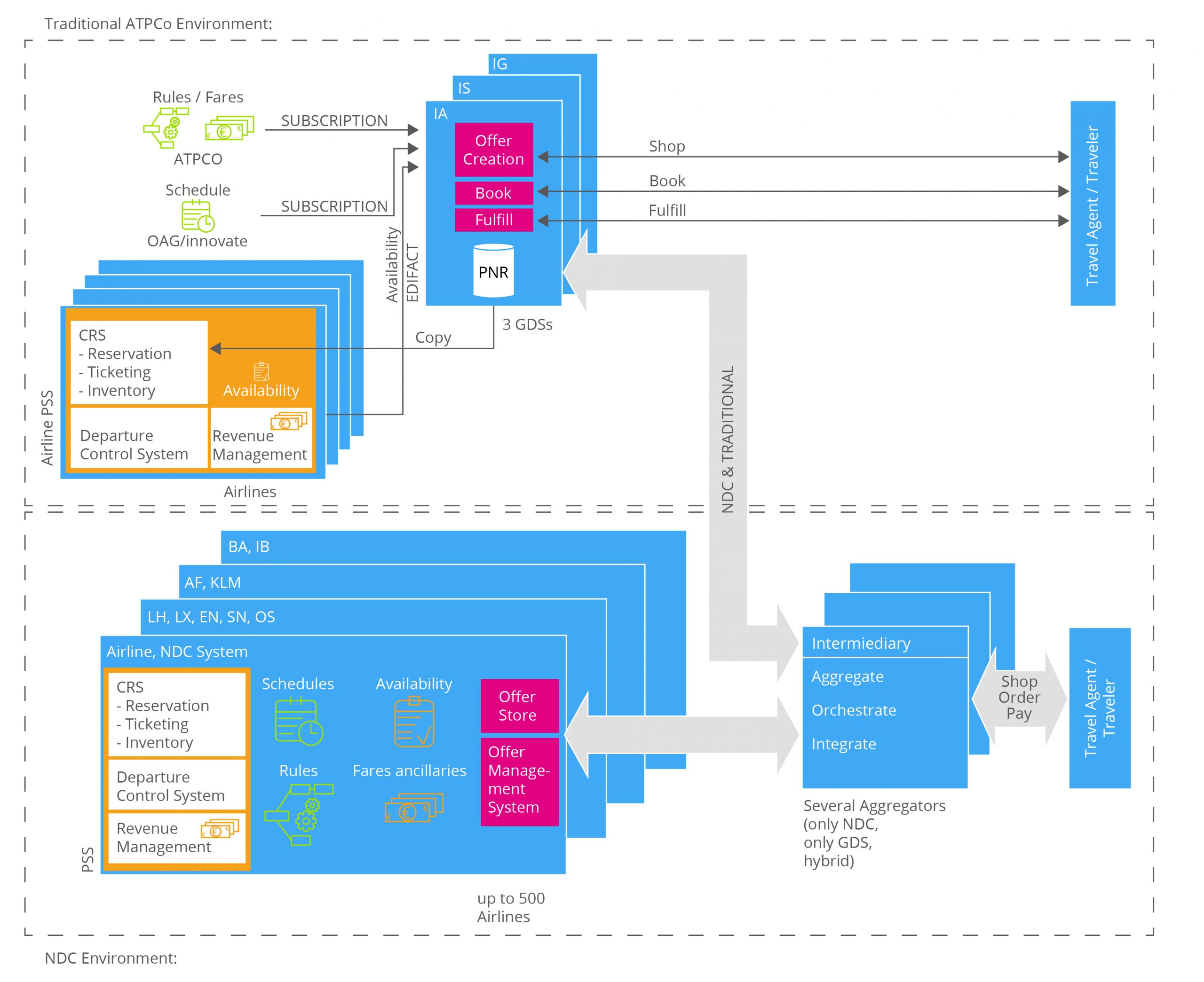

NDC as the Standard for Airline Distribution in the 21st Century Will Become Reality as a Hybrid NDC and ATPCO Model:

In the following, you will find a comparison of the traditional ATPCO based distribution environment to the new NDC based distribution environment. I’m fairly certain that both workflows will remain around for at least until I retire.

On the top, the traditional distribution workflow with a communication protocol which is sometimes still based on the over 40 yr. old EDIFACT protocol and a workflow which is based on ATPCO (filing of fares through ATPCO limited to 26 price points of the alphabet instead of airline offers allowing continuous pricing based on supply and demand at the time of shopping/booking).

On the bottom the new NDC workflow where shopping occurs in the airline offer store (not the GDS) based on supply and demand at that time and the booking occurs directly in the airline order management system. Both models will coexist for a while and intermediaries will have to manage to support both workflows.

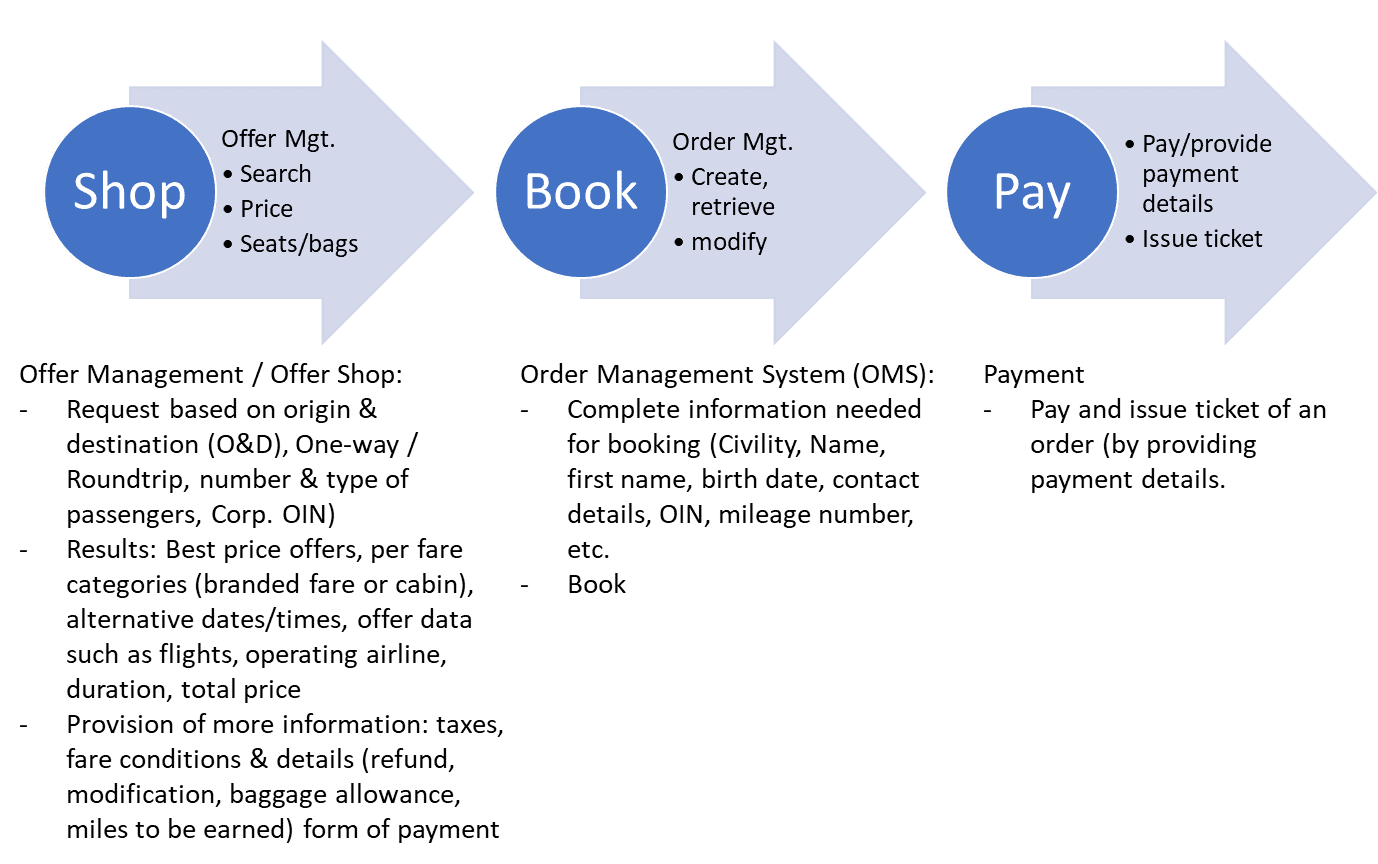

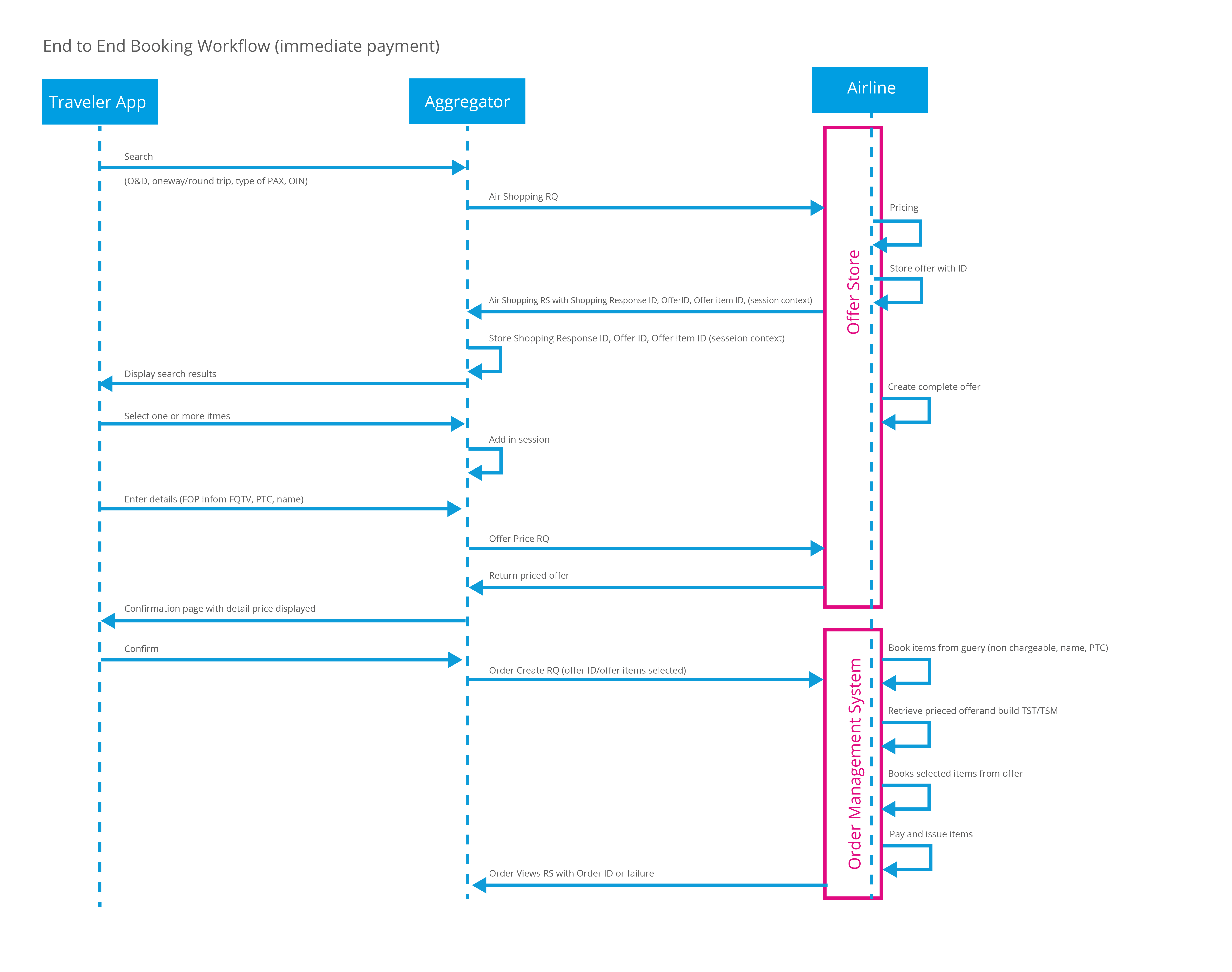

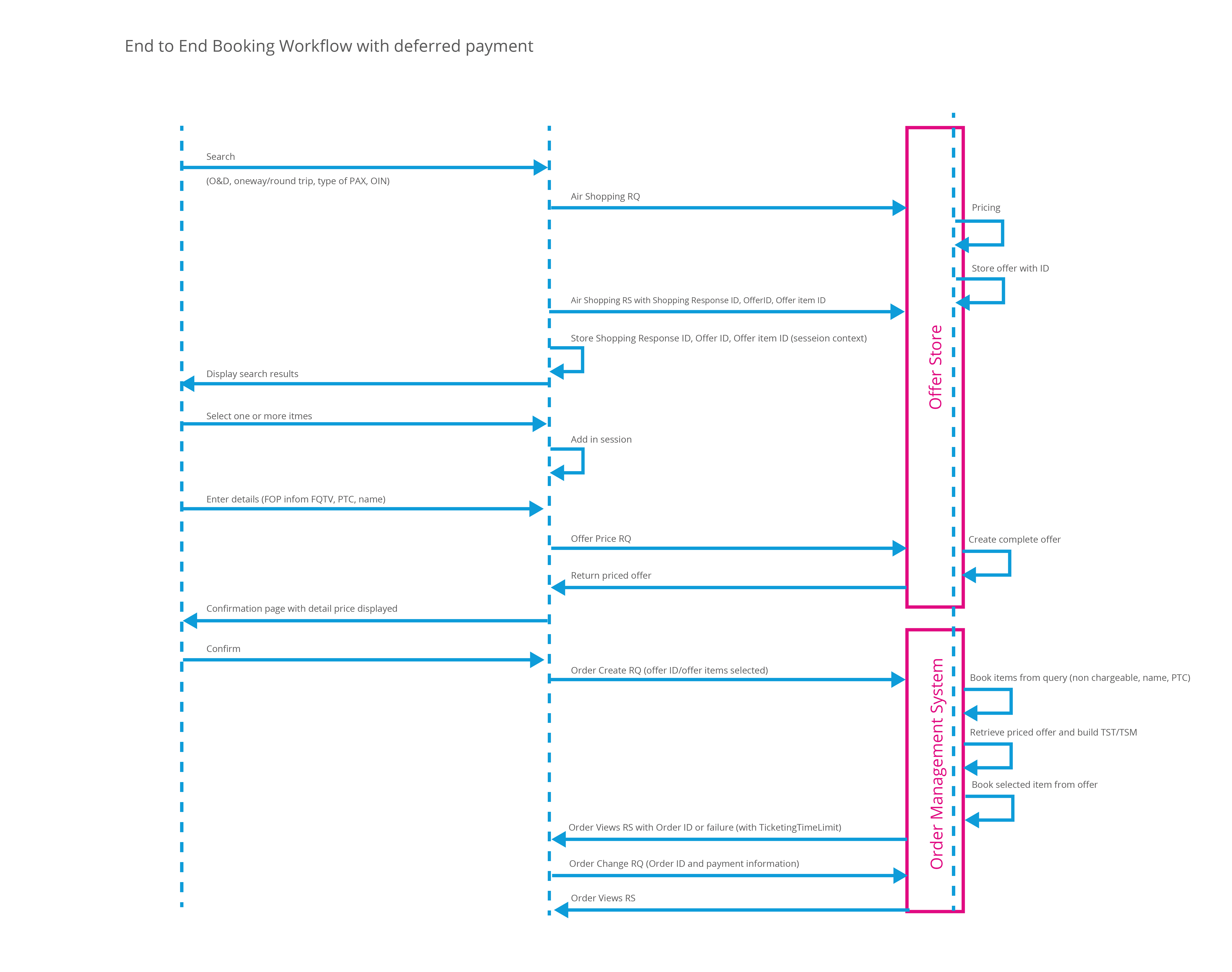

A Typical NDC Booking Workflow

The NDC booking and ticketing workflow consists of three main areas:

Shop (search & price of flights, seats, baggage and services) as part of the Offer Management System (OMS):

- Air Shopping: Request Offers for flights on a specific route/date combination (Flight Search using search parameters);

- Offer Price: Reprice Offer and request upsell offers to account for e.g. updated exchange rates (OfferPriceRQ is always requested using References such as OfferID, OfferItemID);

- Service List: Request available Ancillary Offers; The ServiceList returns chargeable ancillaries. Additional SSR requests can be entered via Augmentation Point;

- Seat Availability: Request Seatmap with prices (if applicable);

Book (create, retrieve & modify orders) as part of the OMS:

- Order Create: Create the booking (if FOP – Form of Payment – is included, documents may be issued automatically). FOP is the trigger for ticketing in Order Create or Order Change;

- Order Reshop: Reprice existing Order, repricing taxes/fees;

Pay (travel documents issuance, retrieval and payment):

- Order Change: Send payment detail (FOP) and trigger payment/ticketing along with EMDs;

Other items such as airline profile & misc. stuff can follow after these steps.

Accomplishments Expected with NDC

With the help of NDC, airlines are primarily trying to differentiate one from another, however, there are a few additional achievements.

Personalization: such as enhancing loyalty with personalized pricing offers (e.g. frequent flyer status may enhance an offer by tier or service experience), but also by enhancing its CRM to be able to propose tailor-made offers which could lead to improved look-to-book ratios and strengthen customer loyalty for future sale. From a customer perspective: Relevant content (“Understand me!”), smart content (“Recognize me!”), complete content (“Service me!”) and easy (“Facilitate me!”).

Differentiation: ability to show competitive features that may be unique to the offer and therefore drive purchase decisions.

Merchandising: displaying additional products (ancillaries) à la carte or bundled (for instance: Wi-Fi or lounge access may drive purchase decisions and/or generate additional revenue for the airline).

Rich content to inspire: instead of a seat on an airplane, airlines want to sell an experience fitting their brand. In the traditional channels, traditional airlines were unable to differentiate their products, which eventually caught them in a commodity trap and a race for the cheapest fare. Especially with low-cost carriers, it is hard for traditional airlines to compete. In the old days, the business and first-class clients presented airlines with lucrative profits, but prior to Covid-19, the back of the aircraft paid the bills. In today’s world of high resolution image or video information at everyone’s fingertips, lie-flat seats, an appealing meal, a top-notch modern cabin, or just a cleaner, truly sanitized and/or social distancing accommodating interior can only be sold via rich content and attractive product presentation. Airlines sell via impressions on their websites, so they need to be able to reach the traveler the same way through their indirect sales channels. In a post-Covid-19 world, this might be even further important as traveler want to see how they can sit in a distance to the neighbor and what measures have been taken to avoid contamination.

Dynamic continuous pricing conductive to modern offer management: flexible prices for products or services based on competition, supply and demand which do not require fare filing. With that said, airlines might have to file fewer fares as if they rely on classic dynamic pricing, hence the current fare filing processes can be simplified and therefore the airlines use this argument to gain NCD traction saying it leads to lower costs.

Control the offer/sale: as the airline produces the offer and is responsible for booking and ticketing, it manages more closely how its product is sold with less risk of interference. Hence, numerous revenue integrity checks may become redundant. In an NDC world, the airlines also carry the true PNR (or order for that matter), and not just a copy of the GDS PNR like in the traditional ATPCO based distribution channel. This fact seems a little scary for the classical GDSs as they lose control (and actually need to find out, how to get the real truth back into their system and synchronized the airline order to their system) – a fairly new thinking process for the GDSs. Not so much for the aggregators (incl. ourselves), as aggregator always had to worry about where the true PNR (or order in the new world) is stored and synchronize prior to making adjustments to the order. For classical GDS aggregators not much changes, as all they have to worry about is if they create a PNR in a 3rd party system called GDS or an order in a 3rd party NDC system of an airline.

Flexibility of the sale: in the past, airlines were restricted in their flexibility to sell. The selling capabilities are simplified with NDC, new products can be introduced much faster (Time to Market), offers can be bundled to the liking of the airline, and upselling (e.g. fare families) by, for example, displaying multiple price points, with increased value, may drive additional business and better sales of higher class features to the airline. All this comes at a downfall, as it obviously makes it much harder for the consumer to compare apples to apples. I guess it comes down to the Travel IT provider to come up with smart solutions to compare – such as the Next Generation Storefront (NGS) by ATPCo’s Routehappy in order to bring consistency to how product offerings are displayed across the airline distribution ecosystem. The disadvantage is only that every such technology comes at a price, and the content is only as good as it is maintained – which is not always dead-on. I’m still trying to picture how advertising financed user generated content (UGC) can wrap this up. In a post COVID-19 world, such content also needs to include COVID-19 testing, border control and vaccination requirements at the time of booking.

Interlining: NDC promises simplified interlining along with a transformation into a revenue opportunity. When an offer needs to be completed by a partner, this can be done dynamically. The partner can make its own offer for their part and seamlessly integrate into the Offer Responsible Airline (ORA). Airlines may not need to file interline agreements as before. Interline settlement disputes could disappear as settlement values are communicated and agreed upfront at time of shopping. However, I consider this also debatable, as then each airline could have to integrate with each other and that might also cost and create conflict. Just imagine, a traveler being able to have two free pieces of luggage with one airline but only one piece on the other airline. Until this all is working seamless with all aggregators, I can see passengers being stranded, where an airline requires that passenger to check or gate-check his luggage at a stopover. In the end, it is up to the airline to decide and one can say: at least now, an airline who wants to integrate with one another can do so.

Reach: increasing reach such as tapping new sales channels geographically and digitally; Reach may be a controversial benefit as it is obvious that GDSs have a pretty high reach. Why else would the largest US domestic airline (Southwest) who has historical not been in the GDS enter the GDS world? IATA claims that direct connect and new aggregators may increase the reach. On the other side, with the multiple adapters to be built, “reach” – especially in the beginning of NDC is debatable and seems rather like a theoretical marketing claim by IATA.

Complexity Reduction: according to IATA, standardization means a common API, which could mean less complexity. This argument I’d like to challenge: IATA proposes two new versions per year, some airlines might adopt new versions, other not. In addition, the standard is not unified and each airline may interpret certain structures differently. Example: A stopover entertainment program by Lufthansa in Munich (e.g. visit a brewery) might be differently implemented by American Airlines to visit the Cowboys in Dallas. Now we have a multidimensional IT challenge: aggregators have to integrate x airlines using y versions of NDC with z interpretations of certain fields.

Payment innovations: with airlines in control of the payment, airlines might further cut costs by introducing payment instruments such as PayPal, Bank transfer, Pay by installment, Air Miles, or Cash to avoid the up to 3% credit card fee.

What Are the Drivers Behind NCD?

- The capability of airline websites is constantly improving. Airline retailing is following the online selling standards of the retail industries. For instance, one can purchase airline ancillaries such as seats, baggage, meals or lounge access as well as 3rd party ancillaries such as hotels, rental cars, local entertainment, etc.

- The Passenger Service Systems (PSS) consisting of inventory, reservation, departure control, etc. that were built in the 1970s by airlines in house have been replaced with systems provided by 3rd party IT providers with many more capabilities.

- The Consumer better understood with CRM tools along with analytical capabilities for personalization and tailor-made solutions.

- The modernization of 40-year-old data exchange standards for ticket distribution developer before the internet was invented. This will make change more cost-effective.

- Besides the GDSs, the facilitation of new entrants was expected to increase competition and drive down cost. It remains to be seen how Covid-19 affected those new entrants and as at length discussed in my other NDC articles bringing together numerous airlines and multiple TMCs/corporates on a technical as well as commercial level is quite a challenge.

- NDC is expected to provide airlines with cost optimization opportunities in the areas of ticketing, payment, revenue accounting, back-office and fare auditing.

Travel agency landscape

- OTAs and metasearch have grown, allowing a much larger number of offers to be processed.

- TMCs have evolved moving to a service-oriented model (duty of care, etc.), partnering with OBTs and mobile solution providers.

- Agents are confronted with a highly educated traveler and an increasing complexity of sourcing content, and thus have a need for intermediaries that fully aggregate content.

- Satisfy the traveler and the corporation in a convenient and simple way.

- Be able to control.

- Security and duty of care.

- Be able to book fares enriching the official corporate channel to satisfy travelers while maintaining their corporate travel policy.

| Indirect Distribution | Traditional ATPCo based environment | NDC environment |

|---|---|---|

| Shop | GDS creates offer usually getting fares and rules from a 3rd party such as ATPCo, schedules from OAG or Innovata, availability by hooking into the PSS (Altea, Sabresonic, etc.) via EDIFACT. | The intermediary (“Aggregator”) – which could be a GDS but does not have to be – transmits the shopping request to one or more airlines via XML using the IATA proposed schema supported by the airline (e.g. 17/2 or 18/1, etc.). An aggregator needs to be integrated with at least one current version of the respective airline, and it usually includes a certification with each airline the agency wants to shop. The Offer Store of the airline creates the offer based on prices, products & availability, which is presented to the traveler/travel agent. The aggregator aggregates the offer(s) of various airlines and presents them to the traveler/travel agent. Once an offer is selected, additional items such as seat, baggage and ancillaries can be added and repriced. |

| Book | GDS creates the PNR which belongs to the Travel Agency and is stored in the GDS. The airline only owning a (partial) copy of the PNR. | When an offer is selected by the traveler/travel agent, the aggregator sends a create order request to the Offer Management System of the airline, who owns the order. |

| Fulfillment: payment & ticketing | Payment (two processes): 1. money is collected by the travel agent using its merchant of record and then settled with the airline at a later stage using a mechanism called e.g. Billing and Settlement Plan (BSP). In this case, the travel agent bears the cost of settlement and remittance (approx. 10 Cents). The airline trusts the agency, which has gone through an accreditation process. 2. In the pass-through process, the travel agent uses a GDS and enters the customer card details. The GDS will then proceed with the payment authorization. No money is collected by the travel agent. The card payment will be credited to the airline bank. The airline bears all payment costs for the reporting of the payment transaction (BSP) as well as the card cost. The airline uses its own merchant of record. Payment costs are estimated at $7 B to the industry (a $350 ticket may be $0.10 for BSP/ARC and $10 for the card). Ticketing: Once payment has been accepted, the agency asks the GDS to initiate a ticket issuance with the airline. The GDS verifies airline is authorized to ticket with this agency, applies a neutral ticket number and sends it to the ticketing airline. The airline validates sufficient data and confirms to agency via GDS. | Payment: The order is created e.g. with PCI compliant credit card data. The intermediary/aggregator does not collect the payment authorization but simply passes on PCI compliant payment details to the airline using the “order request” that will trigger the creation of the PNR and e-ticket, or the Order. The airline processes the payment as according to IATA, besides being the actual contractual partner to the transaction, the airline is better positioned to manage payment as it can accept / refuse a specific card and process fraud detection similarly to its direct sales. Airlines may want to apply a bigger payment portfolio of payment instruments such as - PayPal - Bank transfer - Pay by installment - Air Miles - Cash - New or local forms of payment Payment instruments are fueled by the FinTech community, and thus the traditional environment seems lagging behind in the view of airlines. Transfer will be instant in Europe, within the framework of Regulations (PSD2), removing the current airlines specific complexity to have the PNR on hold. Ticketing: Agency and airline work directly together. When airline is satisfied with the proposed payment, it issues the travel documents and sends the references to the travel agency. |

Compatibility

| Indirect Distribution | Traditional ATPCo based environment | NDC environment |

|---|---|---|

| Reporting | Standard reporting through IATA or ARC. | IATA Billing & Settlement Plan (BSP) came up with a New Generation of IATA Settlement Systems (NewGenISS) to offer risk management between airlines and agents and avoid bilateral individual arrangements. ARC also provides help with regard to NDC implementation. |

| Interlining | GDS constructs interline itineraries and applies filed fares. Each participating carrier has little control of the revenue to expect (using industry proration rules or bilateral agreements) until the flight departs. | While creating an offer, an airline may include services of other airlines. The so-called Offer Responsible Airline (ORA) is responsible for obtaining content from its own interline partners called Participating Offer Airline (POA). |

| Servicing | Changes are carried out by the GDS. | The core NDC principle is that the airline is in control of its distribution. Bookings (Orders) are made in the airline IT environment. Agents can access an order directly in the airline environment instead of the GDS. |

Examples of Typical NDC Booking and Exchange Workflows

Disclaimer: Flow charts are for illustration purpose only. Always check with your NDC airline for up-to-date information. No warranties are made that flow charts are correct.

For Ancillaries NDC Allows Three Options:

- During Booking: Air Shopping à Offer Price (optional) à Service List à Offer Price à Seat Availability à Offer Price à Order Create;

- Post Booking: Order Retrieve à Service List à Seat Availability à Offer Price à Order Change

- Post Ticketing: Order Retrieve à Service List à Seat Availability à Offer Price à Order Change (same)

It seems like some airlines allow services and seats in some cases only after ticketing – which is confusing, as at some point ticketing is supposed to be eliminated. Also, when using deferred payment, certain airlines restrict ancillary services to be added at the Order Create step. In these cases, ancillary services can only be added once payment is made. During booking, such services only seem to be allowed if they are accompanied by a payment guarantee. Again, depending on the implementation this may be combined with an EMD and if so, EMDs in NDC are non-refundable, which might be areas for disputes.

For aggregators who want to mimic the traditional ATPCO workflow in order to be backwards compatible with their clients who will use a hybrid model, it may be necessary to only allow ancillaries after ticketing.

Airline Retailing Maturity Index

- Capabilities verification: Capabilities enabled by the IATA standards

- Partnerships deployment: Scalability across the retailing value chain

- Value capture compass: Maturity of capturing potential value

The second pillar, “Partnerships Deployment” is designed to give airlines and vendors insight into how well they are doing in scaling their NDC-supported capabilities. To do this, airlines and their vendor partners provide IATA with information on the extent of their partnerships.

The third pillar, “Value Capture Compass” is for airlines only. It is designed to help them understand how they compare to their peers in implementing modern retail strategies – such as bundling products and content, pricing and yield management, customer loyalty and payments.

The transition to the ARM Index is expected to be completed by the end of October 2022, when the old NDC register will be shut down.

PASS Travel Agent Desktop

Cover: Shutterstock

This Post Has 2 Comments

Thank you for your comment. I appreciate that. This is a good question. And no, the answer is “I do not believe that an airline will pay any GDS any money in an NDC environment”. An agency will have to recover fees from the traveler (or strike a deal directly with the airline), and the GDS will have to factor in their contracts with the airline as well as with the agencies the fact, that they will not receive commission & overrides (https://www.travel-industry-blog.com/travel-technology/travel-technology-for-dummies-what-are-incentives-commission-overrides/) from the airline any longer.

Hi Michael,

Thanks for the article – just wondering if you have an updated view on how you think the Unit economics are going to turn out like in this new Hybrid channel vs the traditional GDS channel?

Taking an example for the traditional GDS channel today, If a customer buys a $250 air ticket, the airline pays a $5 booking fee to the GDS and the GDS pays a $2.50 incentive fee to the Travel Agent, it results in a $2.50 gross profit for the GDS (50% Gross margin). What would this same transaction look like within the Hybrid NDC model noted above?

I guess what I am trying to understand is whether or not the GDS is still going to be paid for what it does in the channel and if it is getting paid, will it be more or less?

Thanks